Introduction

Running a business comes with a long to-do list. From managing inventory to keeping clients happy, your hands are always full. But if you are registered under the Goods and Services Tax (GST) regime in India, there is one critical financial concept that you absolutely cannot afford to ignore: the Input Tax Credit (ITC).

Think of Input Tax Credit as a financial fuel injection for your business’s cash flow. In plain terms, it allows you to deduct the tax you have already paid on your business purchases from the tax you owe on your sales. However, as many startup founders and small business owners quickly realize, navigating the GST portal and staying compliant with the tax laws can feel incredibly overwhelming. One simple clerical error or a delayed invoice submission by your supplier can lead to a blocked claim, an unwanted tax notice, or extra out-of-pocket expenses.

If you have ever felt confused by the matching of invoices, time-barred claims, or the fear of getting an automated department notice, you are in the right place. In this ultimate guide, we are breaking down the GST Input Tax Credit Rules Every Business Should Know. By the end of this article, you will have a clear, actionable understanding of how to protect your business profits, navigate monthly compliance easily, and maintain perfect records.

What Is Input Tax Credit (ITC)?

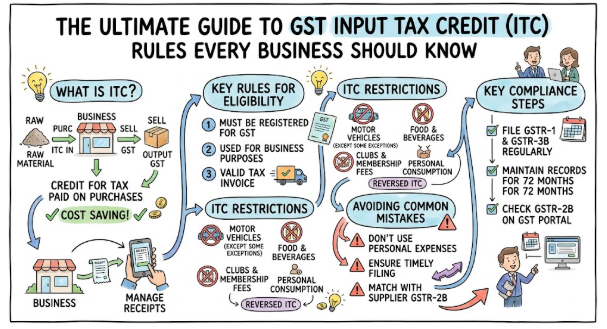

To understand GST ITC rules, let’s strip away the legal language and look at the core concept. When you run a business, you buy raw materials, equipment, office supplies, or services (like internet packages or legal advice) to keep your operations running. Whenever you buy these inputs, your suppliers charge you GST. This tax paid on your business purchases is called Input Tax.

On the flip side, when you sell your goods or services to your customers, you collect GST from them. This is your Output Tax Liability, which you are legally required to pass on to the government.

Input Tax Credit (ITC) is the mechanism that lets you adjust the Input Tax you have already paid against the Output Tax you have collected. Essentially, you only pay the net difference to the government.

This setup prevents the “cascading effect” of taxes, which is just a fancy way of saying “tax on tax.” Without ITC, goods would become progressively more expensive at every stage of production and distribution, hurting both businesses and final consumers.

How ITC Works in GST

Let’s see how this plays out in a normal, day-to-day business scenario. Imagine you run an electronics retail store.

- Your Purchases: You buy 100 premium headphones from a distributor for Rs. 1,00,000. The distributor charges you an 18% GST rate, which amounts to Rs. 18,00, added to your invoice. You pay Rs. 1,18,000 in total. This Rs. 18,000 is your Input Tax Credit.

- Your Sales: Over the next few weeks, you sell those same headphones to retail customers for a total of Rs. 1,50,000. You collect 18% GST from them, which equals Rs. 27,000. This is your Output Tax Liability.

- The Settlement: When it’s time for your monthly GST return filing ITC adjustment, you don’t need to send the full Rs. 27,000 to the government. Instead, you subtract your available credit:

$$\text{Net GST Payable} = \text{Output Tax Liability} – \text{Input Tax Credit}$$

$$\text{Net GST Payable} = \text{Rs. 27,000} – \text{Rs. 18,000} = \text{Rs. 9,000}$$

Instead of making a massive cash payment, you write a check to the government for only Rs. 9,000. This clears your liability smoothly. Friendly reminder: This credit mechanism directly impacts your monthly cash flow, making precise ledger tracking absolutely essential.

Eligibility Criteria for Claiming ITC

While the concept sounds simple, you can’t just claim credit on every single receipt you collect. The government has established clear rules regarding ITC eligibility. To claim input credit legally, you must satisfy all the primary conditions laid down under Section 16 of the CGST Act:

- Possession of a Tax Invoice: You must hold a valid tax invoice, debit note, or bill of entry issued by a registered supplier. A simple cash memo or delivery challan won’t cut it.

- Receipt of Goods or Services: You must have actually received the goods or services. If you pay an advance but the items haven’t arrived at your warehouse yet, you cannot claim the ITC until the delivery is complete.

- Supplier Paid the Tax: The supplier must have actually deposited the tax collected from you with the government, either via cash or through their own utilization of ITC.

- Filing of GST Returns: You must regularly file your own GST returns, specifically the GSTR-3B form.

- Reflected in GSTR-2B: The invoice details must be correctly uploaded by your supplier in their GSTR-1 form, which then populates your auto-generated GSTR-2B statement. If it isn’t visible in your GSTR-2B, you generally cannot claim it.

Important Note: Keep in mind that your true ITC eligibility, valid claims, and required reversals depend strictly on current GST law, your business turnover, and the specific type of supplies you handle.

Documents Required for ITC

To maintain clear audit trails and shield your business from compliance risks, you need robust ITC documentation. If a tax inspector ever reviews your books, you must produce these specific legal documents to support your claims:

- Tax Invoice: Issued by the registered supplier containing their GSTIN, your GSTIN, a sequential serial number, place of supply, description of goods/services, and tax breakdowns (IGST, CGST, SGST).

- Debit Note: Issued by the supplier if the original invoice value was understated.

- Bill of Entry: Required for customs clearance when importing goods into India.

- Revised Invoice / Invoice Issued under Reverse Charge: If you are paying tax under the Reverse Charge Mechanism (RCM), you must generate the payment voucher or invoice yourself to validate the credit.

- Document Issued by an Input Service Distributor (ISD): Relevant for corporate offices distributing input credits across multiple operational branches.

ITC Claim Process

The path to a successful GSTR-3B ITC claim requires a well-structured step-by-step monthly routine. Here is exactly how to claim input tax credit without breaking a sweat:

Step 1: Gather and Record Your Purchase Invoices

As purchases occur throughout the month, log them diligently into your accounting ERP system. Ensure that tax amounts are categorized correctly under CGST, SGST, and IGST components.

Step 2: Access Your GSTR-2B Statement

Around the 14th of the following month, log into the official GST portal and pull up your auto-generated GSTR-2B statement. GSTR-2B acts as your static master reference sheet, locking in the data uploaded by your suppliers.

Step 3: Run a Strict Reconciliation

Compare your internal purchase ledger against the data visible in GSTR-2B.

- Perfect Match: These are ready to claim.

- Missing from GSTR-2B: Follow up with your suppliers immediately. Ask them to file or amend their GSTR-1 so you can claim the credit next month.

- Mismatched Values: Check if there are discrepancies in taxable amounts or tax rates.

Step 4: Account for the Invoice Management System (IMS)

The GST portal uses an Invoice Management System (IMS). This system allows you to formally Accept, Reject, or mark an invoice as Pending. Accepting the invoice ensures it flows seamlessly into your eligible credit pool for the month.

Step 5: Fill Out and File GSTR-3B

Enter your eligible ITC values into Table 4 of your GSTR-3B return. Offset this credit against your output liabilities, settle any remaining balance through your cash ledger, and submit the return by its monthly due date (typically the 20th of the following month).

Common ITC Errors

| Error | Why It Happens | How to Avoid |

| Missing invoice | Invoice not received from the vendor or not recorded in your software. | Establish a central repository for all incoming digital and physical bills; verify all supplier invoices regularly. |

| Incorrect GST rate | Wrong tax code or percentage applied during internal data entry. | Check invoice line items carefully against current GST slabs before recording vouchers. |

| Wrong supplier GSTIN | Typing or entry mistakes made when setting up vendor profiles. | Verify the supplier’s active GSTIN on the portal search tool before finalizing your entries. |

| Claiming ITC on blocked goods | Unawareness that certain purchases are legally restricted from credit. | Check GST law restrictions routinely and consult Section 17(5) lists. |

| Duplicate ITC claim | Multiple accounting entries generated for the exact same invoice number. | Reconcile internal ledger logs with accounting books regularly; implement software alerts for identical invoice numbers. |

| Late ITC claim | Filing delays or missing the statutory annual cut-off timeline. | Track aging invoices systematically; claim credits within the legally prescribed timeline. |

Restrictions and Exceptions: Blocked ITC

It is a common misconception that every single business expense qualifies for tax credits. The GST framework outlines very explicit restrictions under Section 17(5), universally known as blocked ITC. You cannot claim tax credits on the following items, even if they were bought for business purposes:

- Motor Vehicles for Passenger Transport: Generally blocked unless used for driving schools, onwards transportation of passengers, or goods freight services.

- Food, Beverages, and Catering: If you order lunch for a corporate meeting, or cater an annual office party, the tax paid on those catering bills cannot be claimed.

- Club Memberships and Fitness Facilities: Corporate gym memberships, club entry fees, or health spa packages for employees are explicitly blocked.

- Travel Benefits for Employees: GST paid on vacation packages, leave travel concessions (LTC), or personal travel is ineligible unless mandated by statutory employment laws.

- Works Contract for Immovable Property: If you construct an office building or warehouse, the GST paid on civil construction contracts and raw building materials is blocked (unless it’s for plant and machinery installations).

- Lost, Stolen, or Destroyed Goods: If inventory is written off due to theft, fire, or damage, any input tax credit previously claimed on those goods must be reversed.

- Gifts and Free Samples: Items distributed as promotional items or free commercial samples do not qualify for credit.

Practical Tips to Claim ITC Correctly

To maximize your eligible credits while avoiding friction with tax authorities, integrate these fundamental GST compliance tips into your regular financial workflow:

- Implement a 180-Day Payment Tracker: Under GST rules, you must pay your supplier the invoice value plus tax within 180 days from the invoice issuance date. If you fail to pay them within this window, you must reverse the claimed ITC with interest. Always double-check your invoices to ensure payment terms are met on time.

- Enforce Supplier Accountability: Make it a corporate policy to deal only with highly compliant vendors. If a supplier regularly forgets to file their GSTR-1, your cash flow will stall because you cannot claim those credits.

- Separate Personal and Business Expenses: If you buy a laptop for your child’s schooling using the business bank account, do not include that invoice in your business GST fillings. It is a strictly personal expense.

- Maintain Clean Digital Archives: Store physical invoices neatly, and back them up securely in a cloud folder. If you ever face an audit, quick access to clean records saves massive amounts of time and stress.

ITC Reversal and Adjustment Rules

Sometimes, a credit that was perfectly valid when you first claimed it must be reversed later due to changing business conditions. Understanding GST ITC rules regarding reversals prevents bad ledger balances down the road.

Common Reversal Situations

- Non-Payment to Vendors: Reversing credit on bills left unpaid past the 180-day mark.

- Inputs Used for Exempt Supplies: If you use raw materials to produce both taxable items and tax-exempt goods, you must calculate and reverse a proportionate amount of ITC (governed by Rules 42 and 43).

- Personal Use of Assets: If a business asset (like an internet connection or company car) is split 60/40 between business operations and personal convenience, 40% of the associated input credit must be systematically reversed.

The Financial Time Bomb: Section 16(4)

You cannot hold onto old invoices indefinitely and claim them years later. The maximum window to claim missed ITC for any given financial year closes on the earlier of two specific dates:

- November 30th of the following financial year.

- The actual date of filing the GSTR-9 Annual Return for that specific financial year.

If you miss this firm cut-off date, the credit becomes time-barred, and you lose it permanently.

Your Monthly ITC Compliance Checklist

| Checklist Point | Status |

| Supplier invoices verified for correct GSTIN and business details | [ Yes / No ] |

| GST rates charged match current official tax slabs | [ Yes / No ] |

| GSTR-2B monthly reconciliation completed completely | [ Yes / No ] |

| Only eligible ITC selected for final inclusion | [ Yes / No ] |

| Blocked ITC under Section 17(5) completely identified and avoided | [ Yes / No ] |

| Verified final eligible credit values are entered correctly in GSTR-3B | [ Yes / No ] |

| Supporting documents (Invoices, Bills of Entry) retained safely in files | [ Yes / No ] |

| Payments to suppliers tracked to ensure compliance with the 180-day rule | [ Yes / No ] |

| Required reversal entries for personal use or exempt goods checked | [ Yes / No ] |

| Final monthly ledger review completed before freezing accounting books | [ Yes / No ] |

Real-Life Example: The Story of Rohan’s Furniture Business

Let’s look at a practical example of how these steps work in real life. Meet Rohan, the proud owner of Comfort Spaces, a boutique furniture startup in Bengaluru.

Last month, Rohan purchased premium timber worth Rs. 5,00,000 from a local vendor to manufacture office desks. The vendor issued a proper tax invoice charging an 18% GST rate, which amounted to Rs. 90,000 in input tax. Rohan also spent Rs. 20,000 (plus Rs. 3,600 GST) on outdoor catering services for his team’s annual celebration bash.

When filing his monthly returns, Rohan’s accountant sat down to review the files.

First, he looked at the timber invoice. He verified that Comfort Spaces’ correct GSTIN was printed on the bill and confirmed that the timber had arrived safely at their workshop. He checked GSTR-2B and saw that the vendor had already uploaded the invoice. The Rs. 90,000 credit was clean and eligible for use.

Next, the accountant picked up the catering bill. He immediately remembered the blocked ITC rules under Section 17(5). Even though the party was great for team morale, catering tax credits are legally restricted. He set that bill aside and marked it as an ineligible claim.

By staying organized and systematically working through the rules, Rohan safely claimed his Rs. 90,000 credit to lower his cash outflow, kept the catering bill out of his tax filings, and protected his business from compliance notices.

Common Mistakes Beginners Make

If you are new to managing taxes, look out for these typical ITC mistakes to avoid:

- Claiming on GSTR-1 Alone: Beginners often assume that if a bill shows up on their dashboard, they can automatically claim it. Remember, GSTR-1 is just a view sheet; your legal credit must be validated against actual physical receipt of goods and actual business eligibility.

- Ignoring Mismatches: Assuming small discrepancies between your accounting records and GSTR-2B don’t matter is a risky gamble. Over time, these small differences can snowball into major reconciliation headaches.

- Missing out on RCM Duties: Forgetting that if an item falls under the Reverse Charge Mechanism, you must pay the tax out of pocket first before claiming it as an ITC entry in the same month.

- Filing GSTR-9 Late Without Checking Missed ITC: Waiting until the last minute to review your annual records often means missing out on unclaimed credits before the November 30th hard deadline.

Frequently Asked Questions

1. What happens if my supplier does not upload the invoice to the GST portal?

If your supplier fails to upload the invoice, it will not appear in your GSTR-2B statement. Under current rules, you cannot claim ITC on un-uploaded bills. You must contact your vendor and ensure they file their returns correctly so the credit shows up on your dashboard.

2. Can I claim ITC on a laptop purchased for my business?

Yes. If the laptop is used directly for business operations (such as accounting, client communication, or daily work), it qualifies as capital goods, and you can claim the full ITC on it.

3. Can I claim ITC if I am registered under the GST Composition Scheme?

No. Businesses registered under the Composition Scheme cannot claim any Input Tax Credit. They are required to pay a flat tax rate on their total turnover directly out of pocket.

4. Is there a time limit to claim ITC on an invoice?

Yes. The maximum time limit to claim credit on any invoice is the earlier of November 30th of the following financial year or the date you file your annual GSTR-9 return.

5. What is the 180-day rule for ITC?

You must pay your vendor the full invoice amount plus tax within 180 days from the invoice date. If you do not clear the balance within this timeframe, you must reverse the claimed credit along with interest. You can re-claim the credit later once the payment is settled.

6. Can I claim ITC on office rent?

Yes. If the office space is used for business operations and the landlord issues a commercial lease invoice with a valid GSTIN, you can claim the input tax credit on those monthly rent payments.

7. What should I do if I accidentally claim duplicate ITC?

If you mistakenly claim the same invoice twice, you should reverse the duplicate entry in Table 4B of your next GSTR-3B filing. You will also need to pay interest on the duplicate amount if it was used to offset your output tax liability.

8. Can I claim ITC on insurance for a delivery truck?

Yes. While insurance for passenger vehicles is typically blocked, insurance and maintenance for commercial transport vehicles (like a delivery truck or freight carrier) are fully eligible for ITC.

9. What is the difference between GSTR-2A and GSTR-2B?

GSTR-2A is a dynamic statement that changes in real-time as your suppliers upload data. GSTR-2B is a static statement generated once a month (usually on the 14th) that locks in your available data, making it the legal benchmark for matching your claims.

10. Can I claim ITC on office refreshments like tea and coffee?

No. Food and beverage items fall under the blocked credit provisions of Section 17(5). As a result, tax paid on daily office snacks and catering cannot be claimed as an ITC.

Conclusion

Navigating GST Input Tax Credit Rules Every Business Should Know doesn’t have to be a stressful experience. At its core, successful tax management simply requires steady, organized routines. By regularly reconciling your internal ledgers with your GSTR-2B statement, steering clear of blocked credit categories, and addressing vendor filing delays early, you can protect your cash flow and keep your business running smoothly.

Don’t let compliance details overwhelm you. Take it step-by-step: design an internal filing routine, verify your paperwork at each stage, and use our handy monthly checklist to keep your books balanced. If you ever run into highly complex transactions or unique business scenarios, don’t hesitate to reach out to a certified tax professional or a chartered accountant for tailored guidance.

Leave a Reply