Introduction

Many small business owners and mid-sized enterprise founders enter the Indian market with excitement and commercial drive, but they often feel completely confused when tax compliance laws shift beneath their feet. In the early phases of India’s indirect tax journey, an “invoice” simply referred to a physical or digital document created on a local computer, printed out, and handed to a client. However, as the digital core of the Goods and Services Tax Network (GSTN) matures, this traditional practice is no longer legally sufficient. Running a business without understanding these digital updates is like driving on a highway without looking at the signboards—you are bound to hit a structural roadblock.

The primary point of confusion for business leaders lies in the fast-paced lowerings of the legal compliance thresholds. What once applied only to massive, multi-crore conglomerates now impacts everyday micro, small, and medium enterprises (MSMEs) working within regional manufacturing and service supply chains. If your firm crosses the statutory threshold and you continue to issue traditional paper-based or standalone bills without centralized government validation, your business is technically committing a tax offense with every single transaction. Poorly managed billing architectures do more than cause minor internal delays; they quietly erode supplier trust, spark catastrophic capital lockups, and trigger punitive action from regulatory authorities. For an expanding business, an unrecognized or unauthenticated invoice acts as a silent leak through which cash flow, customer relationships, and market authority drain away.

This deep guide is explicitly written to cut through the legal jargon and provide a transparent, step-by-step roadmap to understanding GST E-Invoicing Rules for Indian Businesses. Whether you are a newly registered GST dealer trying to understand your legal boundaries, a corporate accountant auditing fiscal exposure, or a business owner modernizing your enterprise resource planning systems, a clear understanding of these frameworks is essential. Moving forward, digital validation is the only way to protect your commercial ecosystem, fulfill your public obligations, and maintain smooth corporate growth. This blog will explain the mechanics of real-time validation, deadlines, and the practical steps needed to keep your business operating safely.

2. Understanding GST E-Invoicing in Simple Words

Simple Definition

To truly grasp this concept, we must first clear up a massive misunderstanding: E-invoicing does not mean the government’s online portal will generate or build your business invoices for you. Instead, it is a centralized validation network where your pre-existing accounting records are uploaded, checked for standardized formatting, and digitally stamped by an approved regulatory node. Think of it like a passport authentication office. You create the documentation through your own business tools, but the government must verify its parameters before it holds official legal weight across national borders.

How it Works & Where it is Used

Whenever your enterprise sells goods or provides services to another business entity, your billing software outputs a standardized data file format called a JSON payload. This file contains specific line items, tax distributions, and entity identifiers. Your system securely transmits this data packet to a government-designated platform called the Invoice Registration Portal (IRP). The portal instantly verifies that the structure complies with standard national criteria, records the core financial figures, and returns a unique 64-character alphanumeric string called the Invoice Reference Number (IRN) along with a digitally signed Quick Response (QR) Code.

Connection with Money & Real-Life Example

In daily commercial activities, this connects directly to tax flow and customer retention. Imagine an electronics wholesaler issuing a bill for ₹5,00,000 to a retail store owner. Under modern rules, the wholesaler’s system talks to the IRP, fetches the QR code, and prints it on the invoice. Without this digital stamp, the invoice is considered text on paper with no tax value, and the buyer cannot use it to settle accounts.

Common Misunderstanding & Practical Takeaway

A common misunderstanding is that e-invoicing replaces your current accounting software entirely. In reality, your software stays exactly the same; it just learns to talk to the government system. The practical takeaway is clear: e-invoicing creates a real-time, shared ledger between your business accounts, your corporate buyer’s tax ledger, and the central government.

3. Why GST E-Invoicing Is Important

Implementing clean e-invoicing frameworks directly influences your enterprise’s financial stability, risk profile, and cash flow velocity. When your organization embraces an automated verification workflow, the benefits cascade across your accounting ledger:

- Savings: Automating the data transfer from your local system to the central network eliminates the need for manual data entry teams, reducing long-term administrative costs and data correction expenses.

- Tax Planning: Because every outward invoice is recorded on government servers instantly, your end-of-month tax liabilities are calculated automatically, allowing for predictable and error-free tax planning.

- Risk Awareness: It protects your business from massive regulatory penalties. Issuing non-compliant invoices can lead to heavy operational fines that drain company cash reserves.

- Better Planning: Your corporate buyers depend heavily on Input Tax Credit (ITC) to lower their net tax liability. If your billing workflow fails to generate a valid IRN, the transaction details will not automatically populate your buyer’s credit ledgers, allowing you to plan collections better.

- Long-Term Financial Discipline: It forces your business to move away from chaotic, unorganized bookkeeping habits and adopt standardized, institutional workflows that increase the market value of your enterprise.

Short Practical Scenario: Consider a regional packaging firm that switched to real-time e-invoicing. Within two months, their accounting team stopped spending weekends manually correcting monthly mismatch errors. More importantly, their corporate clients noticed that their tax credits reflected instantly, leading to faster payment releases and stronger trade trust.

4. The Real Problem Readers Face With GST E-Invoicing

The real-world friction surrounding GST E-Invoicing Rules for Indian Businesses does not stem from a lack of commercial intent; it comes from a deep gap between changing rules and legacy software systems. Most growing firms rely on outdated offline accounting software or heavily modified legacy ERP configurations. When sudden, strict government rules are introduced—such as the mandatory 30-day reporting window for uploading bills to the IRP—these rigid software frameworks break down completely under the new requirements.

Furthermore, business owners face a constant flood of conflicting, low-quality advice online. Unverified internet forums and social media groups often tell founders that e-invoicing is completely optional for small businesses with lower profit margins, or that formatting errors can be easily fixed long after the financial year ends. This dangerous misinformation leads to poor compliance habits. Teams often ignore mandatory structural fields, skip real-time validation checks, and view e-invoicing as an optional bookkeeping chore rather than a strict legal requirement. By the time a corporate client raises an alarm over a frozen tax credit or an auditor uncovers systematic formatting errors, the business is already exposed to significant penalties and costly operational disruptions.

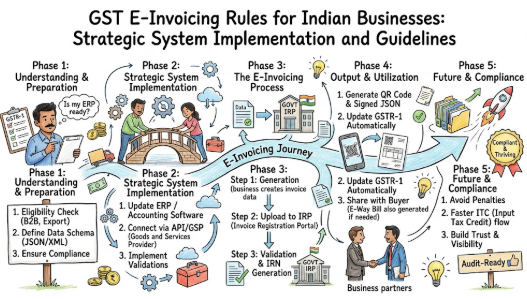

5. How GST E-Invoicing Works Step by Step

Step 1: System Alignment and Data Preparation

- What it Means: Configuring your internal invoicing systems to match the standardized national e-invoice schema (Form GST INV-01).

- Why it Matters: The government IRP servers will instantly reject any upload packet that leaves out mandatory fields.

- How to Apply it: Update your billing database fields to ensure data points like supplier legal names and address structures are locked in correctly.

- Practical Example: An auto-parts supplier adds a dedicated validation field for 15-digit GSTIN inputs into their billing software.

- Common Mistake: Leaving the buyer’s regional PIN code blank or using informal business nicknames.

- Better Approach: Set up automated system blocks that prevent an invoice from being saved unless all mandatory GSTN fields are fully filled out.

Step 2: Generation of the Local Invoice Payload

- What it Means: Creating the financial record within your internal software and compiling the transaction line items into a standard offline JSON data file.

- Why it Matters: This electronic file format serves as the base data layer that your business sends directly to the official validation networks.

- How to Apply it: Enter your raw sales figures, product quantities, and applicable tax weights into your system to let the software automatically generate the structured data packet.

- Practical Example: A garment manufacturer inputs a batch sale of 1,000 shirts, and the software packages the line items into an encrypted JSON data file.

- Common Mistake: Manually editing the text codes inside the JSON file using basic text apps, which corrupts the file’s data layout.

- Better Approach: Trust your integrated billing system to compile the source data automatically, ensuring zero human touch during file generation.

Step 3: Secure Transmission to the IRP Network

- What it Means: Sending the structured data payload securely from your local system to an approved government Invoice Registration Portal (IRP).

- Why it Matters: This step moves the invoice out of your private company books and into the official public validation channel.

- How to Apply it: Use direct, secure API integrations or trusted third-party GST Suvidha Providers (GSPs) to establish a pipeline to government servers.

- Practical Example: Clicking “Approve Invoice” inside an office system sends the data securely to the government server node within two seconds.

- Common Mistake: Relying on slow, manual copy-paste entry methods on web portals during high-traffic end-of-month windows.

- Better Approach: Set up a direct, real-time API connection that uploads your data to the IRP automatically the moment a sale is finalized.

Step 4: Centralized De-Duplication and Validation

- What it Means: The government IRP computers analyze the incoming data packet to verify that the specific document number has never been processed before during the current financial year.

- Why it Matters: This automated gatekeeper check prevents businesses from accidentally uploading duplicate invoice numbers, eliminating double-taxation errors.

- How to Apply it: The portal evaluates the unique combination of the Supplier’s GSTIN, Document Type, Document Number, and target Financial Year.

- Practical Example: The government cloud system checks an uploaded bill numbered “INV-2026-0045” to ensure it hasn’t been logged previously.

- Common Mistake: Trying to re-upload an edited bill using the exact same invoice number after a previous version was already successfully registered.

- Better Approach: If transaction details change, formally cancel the original e-invoice on the portal within the legal 24-hour window, or issue a structured Credit or Debit Note.

Step 5: IRN Generation and Digital Stamping

- What it Means: The official portal successfully registers your transaction data, signs it with a private government key, and generates a unique 64-character alphanumeric Invoice Reference Number (IRN).

- Why it Matters: The generation of this long reference string is the explicit legal proof that the transaction is fully recognized by the state tax authority.

- How to Apply it: Your local accounting system receives the authorized IRN string back from the government servers, saving it directly into that invoice’s database row.

- Practical Example: The server processes the file and returns a unique hash string like

a1b2c3d4...representing that specific business transaction. - Common Mistake: Recording only the first few letters of the IRN string in your local tracking spreadsheets, which makes future audit tracking impossible.

- Better Approach: Ensure your database stores the entire 64-character alphanumeric string automatically, linking it permanently to your internal ledger records.

Step 6: QR Code Reception and Layout Integration

- What it Means: The government IRP server returns a compressed, digitally signed QR code along with the unique IRN string back to your local system.

- Why it Matters: This QR code contains essential transaction data points, allowing logistics teams and field auditors to verify the bill’s validity offline using mobile scanning apps.

- How to Apply it: Your billing system automatically pulls the returned QR graphic data and embeds it onto the layout of the invoice document.

- Practical Example: Your warehouse printing machine receives the server data and prints a sharp, high-contrast QR box on the top-right corner of the shipping page.

- Common Mistake: Scaling down or distorting the printed QR code image onto a tiny corner of the page, which makes it unreadable.

- Better Approach: Reserve a clear, high-contrast block on your invoice print template specifically for the QR code, ensuring it prints perfectly for logistics teams.

Step 7: Automated Return Ledger Auto-Population

- What it Means: The IRP server shares the validated transaction details directly with the central GST portal, automatically filling out your company’s GSTR-1 registry and your buyer’s GSTR-2B credit book.

- Why it Matters: This automated data flow removes the need for manual data entry at the end of the month, completely preventing filing mismatches between buyers and sellers.

- How to Apply it: Review the auto-populated rows in your monthly draft return against your local sales books before clicking the final submit button.

- Practical Example: On the 11th of the month, a business owner opens their GSTR-1 form and finds all their B2B transactions already neatly logged in the tables.

- Common Mistake: Manually overriding or changing the auto-populated values directly within the GSTR-1 web form without correcting your local source data first.

- Better Approach: Treat the auto-populated rows as your absolute source of truth. If any errors are found, use official debit or credit notes to correct the values across both systems.

6. Key Factors That Influence GST E-Invoicing Compliance

Documentation

Standardized formats are absolutely mandatory. Every transaction detail must precisely match official public records, from the accurate 15-character structural breakdown of your client’s GSTIN down to the exact 6-to-8 digit HSN codes for your products.

Filing Accuracy & Record Keeping

The time lag between creating an invoice locally and registering it with the portal must be tightly managed. Validated JSON files, authorized IRN keys, and portal logs must be backed up securely across separate storage servers for at least eight years. Relying on simple paper copies leaves your business incredibly vulnerable during future corporate tax audits.

Compliance Deadlines

For businesses that cross specific turnover limits, missing the strict 30-day reporting window will cause the portal to permanently reject the transaction, rendering the bill legally invalid and causing major friction with buyers.

Penalty Risk

Failing to generate an e-invoice carries heavy financial penalties under Section 122 of the CGST Act. Businesses can face structural fines of ₹10,000 or the total tax amount involved—whichever is higher—for every single non-compliant invoice issued.

Professional Review & Invoice Discipline

Your system configuration needs a regular professional eye. Leaving your billing software unchecked without structural audits can cause systematic formatting drifts that lead to bulk rejections by the IRP validation network.

7. Detailed Breakdown of GST E-Invoicing Rules for Indian Businesses

Basic Meaning of the Topic

GST E-Invoicing is a standardized digital reporting architecture introduced by the Government of India. Under this system, specified business organizations must submit their internal business-to-business bills to a public server for centralized verification before passing the documents to buyers or transportation teams.

Why Compliance Matters

In the modern Indian market, compliance serves as your company’s digital reputation. When your enterprise issues a fully validated invoice with a legal IRN, it signals to financial institutions, corporate clients, and tax authorities that your business operations are entirely legitimate and transparent.

Common Filing or Documentation Mistakes

The most frequent mistake made by growing firms is failing to match product parameters with correct tax brackets. For instance, putting a service tax weight on a physical raw material shipment causes immediate system mismatches that stall your client’s credit matching workflows.

Important Records to Maintain

Your business must maintain a digital archive containing:

- The original government-validated JSON data packets.

- The 64-character alphanumeric IRN strings linked to internal ledger rows.

- High-resolution copies of the printed layouts featuring the official signed QR codes.

Late Filing or Incorrect Filing Risks

If you delay processing an e-invoice beyond your prescribed legal deadlines, the portal will reject the data upload completely. This locks your transaction out of the tax ecosystem, meaning your buyer cannot claim their rightful tax credit and your delivery trucks risk being seized on the road.

Practical Preparation Steps

To ensure error-free daily operations:

- Conduct an audit of your historical business turnover across all regional branch offices.

- Upgrade your billing software platform to a version that supports automated API connections.

- Run weekly training updates for your internal bookkeeping and billing teams.

Difference Between Awareness and Professional Advice

While understanding the basic layout rules helps you monitor daily office tasks, general awareness cannot replace professional guidance. Tax laws feature intricate sub-clauses regarding mixed supplies and zero-rated export structures that require expert handling.

When to Consult a Qualified Tax Expert

You should consult a certified Chartered Accountant or a qualified tax professional whenever you alter your primary corporate business lines, establish a new warehouse facility in a different state, or face a formal compliance inquiry from tax authorities.

8. Common Mistakes Beginners Make With GST E-Invoicing

Why Mistakes Happen & Why They Are Risky

Most operational errors happen because business owners view e-invoicing as a simple administrative chore rather than a strict legal framework. Many founders look only at the turnover of a single regional branch office, completely ignoring that the state tracks aggregate turnover across your entire PAN card, combining all regional branch offices nationwide. This lack of structural awareness can lead to sudden, severe non-compliance penalties when your combined business revenues cross the ₹5 Crore threshold.

What Can Go Wrong

If an internal accounting team discovers an error on a bill three days after generation and simply tries to delete the file from their local database, it creates a massive red flag. Because the original data row remains uncorrected on the central government portal, it triggers automated system audits that can stall your monthly return processing and block your business’s credit filings.

What the Reader Should Do Instead

Instead of trying to hide or delete invoicing mistakes locally, accounting teams must use formal legal correction channels. If an error is spotted within the first 24 hours, the invoice must be officially cancelled on the IRP network. If that brief window has closed, the error must be balanced cleanly by issuing a structured Credit or Debit Note to update the public registers correctly.

The “Don’t Do This” Operational Checklist

- Never issue a B2B sales invoice without confirming that a valid, government-signed QR code is printed clearly on the layout.

- Do not divide your core operating business into multiple artificial sub-firms simply to keep individual branch revenues below the threshold.

- Never use random product descriptions or incorrect HSN numbers just to bypass software errors when uploading data to the IRP.

- Do not allow internal accounting teams to delete or wipe historical JSON data payloads from your local servers after a month’s returns are finalized.

- Never delay uploading a business invoice to the portal past your prescribed statutory reporting windows.

9. Practical Real-Life Examples of GST E-Invoicing Situations

- The Regional Manufacturer: A small automotive components plant logs an annual sales revenue of ₹5.4 Crore. The owner assumes they are too small for complex compliance tracking and continues to send out traditional paper bills. Because they failed to generate an IRN, their corporate clients find their ITC balances completely blocked, causing them to freeze ₹12 Lakh in outstanding trade payments until the bills are properly validated.

- The Branch Office Oversight: A fast-growing logistics enterprise runs three separate branch offices across different states, with each branch generating around ₹2 Crore in revenue. The local accounting team assumes they are safe because no single branch crosses the limit. However, during an audit, the central tax platform aggregates the revenue under their shared PAN card to a total of ₹6 Crore, making e-invoicing immediately mandatory for all three branches.

- The Missed Cancellation Window: A wholesale steel dealer accidentally enters a tax rate of 28% instead of 18% on a major bulk order. The internal accounting team discovers the error three days later and tries to delete it from their local computer. Because the original data row remains uncorrected on the central government portal, it creates a massive tax discrepancy notice during year-end reconciliation.

- The Logistics Transit Delay: An electronics distributor prints out a B2B invoice but scales down the government-returned QR code until it looks like a tiny, blurry square. When the delivery truck passes a highway checkpoint, the officer’s mobile scanning tool fails to read the distorted code, resulting in the vehicle being impounded and a heavy penalty being issued for transporting goods with an invalid invoice.

- The Delayed Portal Upload: A service provider with an annual turnover of ₹12 Crore completes a major corporate consulting project but delays uploading the final billing data to the IRP for 45 days. Because they missed the strict 30-day reporting deadline for businesses in their turnover tier, the portal permanently blocks the upload, leaving them unable to provide their client with a valid tax invoice.

10. Two Useful Tables for Better Understanding

Table 1: Historical Phased Implementation Matrix

| Implementation Phase | Broad Corporate Turnover Limit | Formal Enforcement Commencement Date | Primary Focus Area Across Industry |

| Phase I | Exceeding ₹500 Crore | 1st October 2020 | Massive multi-national entities and large conglomerates |

| Phase II | Exceeding ₹100 Crore | 1st January 2021 | Large national enterprise structures and supply chains |

| Phase III | Exceeding ₹50 Crore | 1st April 2021 | Upper mid-market manufacturing and trading hubs |

| Phase IV | Exceeding ₹20 Crore | 1st April 2022 | Mid-market distribution networks and B2B platforms |

| Phase V | Exceeding ₹10 Crore | 1st October 2022 | Small to mid-sized enterprises across the states |

| Current Phase | Exceeding ₹5 Crore | 1st August 2023 | Core MSME tier, regional suppliers, and service firms |

Table 2: Comparison of Valid Compliance vs. Critical Non-Compliance

| Core Operational Feature | Valid E-Invoiced Document Framework | Non-Compliant Local Invoicing Approach | Systemic Financial Consequence |

| Legal Document Status | Fully valid tax invoice under Rule 48(4) | Legally treated as a failure to issue an invoice | Severe regulatory fines under Section 122 |

| IRP Verification String | Unique 64-character alphanumeric IRN present | Only standard internal invoice numbers present | Complete rejection by institutional audit teams |

| Visible Verification Stamping | Government-signed QR code printed clearly | No official QR code or simple text-only links | Cargo transit teams face vehicle seizure risks |

| Buyer’s Input Tax Credit | Flows automatically into the buyer’s GSTR-2B | The buyer’s credit ledger remains completely blank | Enterprise clients drop non-compliant vendors |

| Reporting Time Tracking | Processed within the strict 30-day window | Exceeds the 30-day portal reporting deadline | The portal permanently blocks the data upload |

Tools, Methods, and Frameworks Readers Can Use

Direct ERP-to-Portal API Integrations

- What it is: A secure database channel that connects your core business accounting system directly with the government’s IRP servers.

- Why it helps: It completely automates the e-way and e-invoice generation process, processing transactions within seconds.

- How beginners can use it: You can enable specialized API modules within modern accounting platforms like Tally Prime, ZoHo Books, or SAP.

- What mistake it helps avoid: It eliminates the need for manual data entry, completely avoiding human typing mistakes and file mismatch errors.

Standardized Government Offline Bulk Utilities

- What it is: A free excel-based data compilation sheet provided directly by the official GSTN network.

- Why it helps: It lets small business owners package an entire day’s sales invoices into a single structured file without investing in expensive custom software setups.

- How beginners can use it: Download the utility template from the public GST portal, input your daily sales rows, and hit the built-in “Generate JSON” button.

- What mistake it helps avoid: It prevents structural filing rejections by verifying that your data aligns with the required formatting rules before you upload it to the portal.

Third-Party GST Facility Providers (GSPs)

- What it is: Licensed external technology platforms configured to act as an optimized data highway into the state tax network.

- Why it helps: They offer real-time data monitoring dashboards, automated tax calculation sanity checks, and secure cloud storage backups.

- How beginners can use it: Connect your existing internal business software with an approved GSP interface to handle multi-branch business data routing.

- What mistake it helps avoid: It prevents data loss and system timeout errors during peak end-of-month upload windows when the primary government web servers experience heavy user traffic.

Expert Tips to Make Better Decisions

- Learn Before Taking Action: Ensure your core invoicing staff completely understand the mandatory schema fields before upgrading your systems.

- Compare Multiple Options: Evaluate different GST Suvidha Providers to find an integrated system that matches your specific business transaction volume.

- Check Risk Before Expected Return: Never choose cheap, uncertified billing software utilities simply to save on setup costs; prioritize system stability instead.

- Keep Written Records: Maintain an organized, secure offline log of all your historical portal communication receipts and error logs.

- Avoid Emotional Decisions: Do not let temporary system implementation delays panic your team into bypassing the portal and issuing unvalidated manual bills.

- Review Your Plan Monthly: Run an internal cross-reconciliation check between your offline sales books and the auto-populated GSTR-1 entries every month.

- Start Small: Run a series of test transactions using the official government sandbox portal environments before taking your new billing systems live.

- Protect Personal Data: Secure your company’s IRP login tokens and private encryption keys with strong, regularly updated security passwords.

- Avoid Fake Promises: Ignore unverified software tools that claim they can legally bypass or backdate the mandatory 30-day portal reporting deadline.

- Read Terms Carefully: Review the data protection clauses and service level agreements offered by your third-party billing software vendors.

- Keep Emergency Money Separate: Maintain a dedicated financial reserve to manage short-term capital gaps if a major client freezes a payment over a billing dispute.

- Take Professional Advice When Needed: Always involve a certified Chartered Accountant when setting up tax parameters for complex, multi-state service operations.

- Do Not Blindly Copy Others: Design an invoice numbering system and document flow pattern tailored to your specific logistics and warehouse realities.

- Focus on Long-Term Discipline: Establish a strict daily office routine requiring all B2B sales records to be uploaded to the portal within 24 hours of generation.

Case Studies: How Better Understanding Changes Decisions

Case Study 1: The Industrial Supplier’s Sudden Turn-Back

- Profile: A precision casting foundry operating out of Coimbatore.

- Situation: The foundry built a strong regional reputation by selling raw components directly to large industrial equipment manufacturers across Southern India.

- Problem: Their accounting team relied on a localized, completely offline desktop database application and ignored the multi-year aggregate turnover rule. They assumed that because their net profit margins dipped during recent market shifts, they did not need to follow the ₹5 Crore compliance rules.

- Wrong Approach: The team ignored automated alerts from their trade partners and continued to mail out traditional, text-based invoices without generating an official IRN.

- Better Approach: After major clients threatened to freeze their supplier status, management halted billing operations, hired a qualified systems integrator, and connected their desktop database directly to an approved IRP server via a secure API utility.

- Result or Learning: The foundry successfully restored its corporate supplier status within fifteen days. The operations team learned that aggregate turnover rules look across your entire historical footprint back to 2017-18, making compliance absolute regardless of short-term profit shifts.

- Key Takeaway: Corporate buyers will rapidly drop non-compliant vendors to protect their own tax ledgers from blocked input credits.

Case Study 2: The E-Commerce Distributor’s Transit Block

- Profile: A consumer electronics distribution firm centered in New Delhi.

- Situation: The firm managed fast-moving consumer orders, shipping large volumes of high-value electronic goods to retail stores nationwide.

- Problem: To save space on their high-volume printing templates, the team modified their software layout, reducing the government-returned QR code down to a small, low-resolution block at the bottom of the packing slip.

- Wrong Approach: Warehouse teams allowed delivery trucks to depart with distorted, unreadable QR codes on the physical paperwork, assuming the text-based IRN string was enough to pass highway checks.

- Better Approach: After a major shipment was detained at a state border checkpoint—resulting in heavy fines and delayed deliveries—the logistics director redesigned the packing template, dedicating a standard, high-contrast block specifically for a clear QR code graphic.

- Result or Learning: Future transit shipments passed through border check-posts smoothly with zero regulatory delays. The company learned that physical shipping documents must feature a perfectly scannable, government-signed QR code to remain legal on the road.

- Key Takeaway: An unscannable or distorted QR code holds zero legal weight during physical transit checks by enforcement officers.

Case Study 3: The Infrastructure Firm’s Deadline Disaster

- Profile: A fast-growing engineering and construction services enterprise based in Hyderabad.

- Situation: The enterprise managed multi-month infrastructure projects, issuing large-value service bills to corporate clients at the end of major project milestones.

- Problem: The enterprise recorded an annual aggregate turnover of ₹14 Crore. Because their billing cycles were spaced far apart, their accounting team routinely delayed uploading completed project bills to the portal, often waiting until quarterly financial reviews.

- Wrong Approach: The team attempted to upload a group of older project bills to the IRP 45 days after their initial document dates, assuming the system would backdate the records automatically.

- Better Approach: The portal’s automated checks instantly blocked the uploads because they exceeded the strict 30-day reporting window for businesses in their turnover tier. The firm had to formally issue structured Credit Notes to cancel the invalid entries, reset their internal invoicing workflows, and establish a strict rule requiring real-time uploads within 48 hours of project milestones.

- Result or Learning: The company eliminated compliance backlogs and secured their clients’ tax credits on time. The team learned that the 30-day portal reporting limit is a hard system rule that cannot be bypassed or overridden manually.

- Key Takeaway: Missing the statutory reporting deadline permanently invalidates a transaction file on the national portal.

Risk Awareness: What Readers Must Check First

Legal and Compliance Risk

Failing to generate an e-invoice when your business crosses the threshold means your invoices are legally treated as non-existent under Rule 48(4). This legal failure exposes your business to immediate fines under Section 122 of the CGST Act. You can reduce this risk by establishing an internal automated checking pipeline that cross-examines branch sales daily against national compliance benchmarks.

Credit and Cash Flow Risk

When you issue unauthenticated billing documents, your clients find their Input Tax Credit balances permanently blocked on the central platform. This breakdown forces corporate procurement teams to freeze your incoming payments or look for alternative compliant vendors. To minimize this exposure, establish a proactive compliance matching framework that verifies portal reflections before shipping products out.

Logistics and Transit Risk

Transporting commercial products with an invoice that lacks an official, scannable government-signed QR code is treated as a major compliance failure by enforcement authorities. State highway check-posts can legally detain your shipping vehicles, seize your commercial cargo, and refuse release until heavy storage penalties are cleared. You can completely neutralize this transit risk by equipping warehouse managers with barcode scanning devices to verify invoice visibility before any cargo truck leaves your warehouse doors.

Checklist Before Taking Action

- Confirm that your business’s accurate 15-character structural GSTIN is updated correctly inside your billing setup.

- Verify your client’s active registration status and corporate name against official records before generating a bill.

- Check that the unique invoice number follows a clean, unbroken sequential series for the current financial year.

- Ensure the correct 6-to-8 digit HSN codes are assigned accurately across all product lines and services.

- Double-check that your tax splits—CGST, SGST, and IGST—are calculated perfectly based on the destination state code.

- Verify that the total transaction value matches your line items exactly, including all shipping fees and regional discounts.

- Confirm that the final structured JSON data payload is securely transmitted to the IRP within the required timeline.

- Ensure the 64-character alphanumeric IRN string is received back from the government servers and saved into your database.

- Check that the official government-signed QR code is printed clearly on the final physical and digital document layouts.

- Back up the validated JSON files and portal logs securely across separate cloud backup servers for your historical records.

This ten-point validation checklist should be positioned prominently on the desks of your billing supervisors. Reviewing these data points systematically before any document is finalized guarantees that your outgoing shipments remain fully compliant, protects your clients’ tax credits, and keeps your business safe from regulatory disruptions.

Strategic Insights for Better Decision-Making

Documentation Discipline

Establishing an unyielding documentation discipline is the absolute foundation of institutional scale. When an expanding company treats every data entry row—from structural corporate state codes to exact product descriptions—with rigorous accuracy, it removes the operational friction that stalls traditional supply chains. This clean accounting data flow helps you avoid sudden audit complications and provides your administrative teams with clean financial records.

Filing Accuracy & Record Maintenance

Maintaining a highly organized, distributed digital archive for your government-signed JSON payloads forms a powerful defense layer during regulatory tax reviews. Moving past simple printed folders and deploying encrypted cloud databases guarantees that your corporate records remain completely secure and accessible throughout the legally mandated eight-year storage window.

Compliance Calendar Planning

Managing your corporate accounting workflow against an active compliance calendar completely eliminates end-of-month processing panics. Setting up automated internal deadlines that ensure billing data packets are transmitted to the IRP within 24 hours of a transaction prevents your system from bumping against the hard 30-day portal reporting limits, keeping your business operations running smoothly.

Key Technical Terms Explained for Beginners

- Invoice Reference Number (IRN): A unique 64-character alphanumeric string generated by the government’s IRP server using a private hashing algorithm. It serves as undeniable legal proof that a specific transaction has been officially registered within the national tax network.

- Invoice Registration Portal (IRP): The specialized, centralized server framework set up by the government to receive, check, and digitally stamp incoming business transaction files in real-time.

- Aggregate Annual Turnover (AATO): The total pan-India revenue generated by a business entity under a single PAN card, calculated by combining all taxable sales, exempt supplies, and export operations across every regional branch office.

- Input Tax Credit (ITC): The legal mechanism that allows a business to subtract the taxes paid on purchases from the total taxes owed on sales, preventing unfair double-taxation across the manufacturing and distribution supply chains.

- JSON Data Payload: A lightweight, highly organized plain-text file format used by modern software platforms to securely exchange financial details and transaction line items between private corporate servers and state tax networks.

- GSTR-2B Credit Ledger: An automated, static tax credit statement generated every month for corporate buyers, serving as their official source of truth to confirm which supplier invoices were properly validated on the portal.

- De-Duplication Routine: An automated security check run by the IRP servers to verify that an incoming invoice number has never been processed before, completely preventing accidental double-billing errors.

- Harmonized System of Nomenclature (HSN Code): A standardized international numerical coding system used to classify commercial products accurately, ensuring uniform tax calculations across all state lines.

- GST Suvidha Provider (GSP): An authorized, secure third-party technology platform approved by the state to provide businesses with user-friendly dashboards and direct API connections to the national tax network.

- Dynamic QR Code Structure: An advanced, interactive quick-response graphic format that contains essential, encrypted transaction data points, allowing logistics teams and field auditors to instantly verify a bill’s validity offline.

Who Should Read This Blog

- Beginners & New Investors: Individuals setting up their very first commercial trading operations who need to map out their tax compliance boundaries before taking on large corporate orders.

- Salaried Employees & Finance Managers: Corporate accounting leaders who need to review enterprise tax exposure risks and implement robust internal data frameworks.

- Small Business Owners: MSME founders whose aggregate business revenues have recently crossed the ₹5 Crore milestone and require a clear compliance roadmap.

- People Improving Money Awareness: Growing business professionals and administrative directors focused on upgrading their bookkeeping workflows to avoid costly legal mistakes.

Frequently Asked Questions

What are the primary GST E-Invoicing Rules for Indian Businesses?

The core rules state that any enterprise with an Aggregate Annual Turnover crossing ₹5 Crore in any financial year since 2017-18 must validate all B2B and export transactions through the IRP.

Does this government system generate invoices for my business automatically?

No, your company continues to create invoices using your own local accounting tools. The government portal simply validates the data format and returns an official digital signature.

What is the biggest mistake to avoid when processing e-invoices?

The biggest error is failing to upload transaction data to the IRP within your prescribed legal deadlines, which can cause the portal to permanently reject your data file.

Is e-invoicing mandatory for basic retail sales to everyday consumers?

No, standard business-to-consumer (B2C) retail receipts are currently exempt from the mandatory IRN generation rules, which apply strictly to B2B, B2G, and export operations.

What happens if an invoice is sent out with an incorrect tax bracket?

The central portal will log the erroneous file. If discovered past the 24-hour cancellation window, the error must be balanced cleanly by issuing a structured Credit or Debit Note.

How can a business check if its current software setup is compliant?

You can run a series of test data uploads using the official government sandbox testing platforms to verify that your system outputs match the required national schema criteria.

Can highway transit officers impound delivery vans for simple printing errors?

Yes, if the physical shipping papers feature a blurry or distorted QR code that scanning tools cannot read, officers can legally detain the vehicle for non-compliance.

Does the aggregate turnover calculation look at individual branch metrics?

No, the state platform evaluates your total combined revenues across all regional offices registered under your unique corporate PAN card.

Can an e-invoice be deleted from the system after a month ends?

No, once an invoice is successfully registered on the portal, its data record is permanently logged in the public archives and cannot be deleted or wiped.

What should a firm do if the primary government servers experience downtime?

You should configure your internal accounting systems to route data packets seamlessly to an alternative government-approved IRP server node to keep operations moving.

Should I consult an external tax professional to review my office setups?

Yes, having a certified Chartered Accountant perform regular quarterly audits of your billing configurations ensures long-term safety and protects your business from compliance risks.

What is the best next step after reading through this guide?

The most effective next step is to run a comprehensive check on your entity’s historical multi-year turnover records to ensure your internal software configurations match your legal requirements.

Conclusion and Next Steps

Navigating the landscape of GST E-Invoicing Rules for Indian Businesses requires a steady focus on technological modernization, strict operational discipline, and an absolute commitment to data accuracy. As the Indian economy transitions toward a completely digital, transparent tax infrastructure, old manual billing habits are fast becoming a major operational liability. Moving forward, digital validation through the portal is the only legal way to safeguard your supply chain relationships, avoid heavy structural penalties, and ensure your corporate cash flows remain secure.

The path to long-term compliance success begins with a clear, honest audit of your current business tools and historical turnover records. Rather than viewing these automated rules as a rigid regulatory burden, smart business leaders treat them as a valuable opportunity to optimize their accounting workflows, eliminate human data errors, and build a highly resilient enterprise. By integrating modern compliance solutions directly into your daily sales operations, your business can step confidently into an automated future—ensuring your enterprise remains fully compliant, highly competitive, and positioned for long-term sustainable growth. Your immediate next step should be to audit your database configurations, update your staff guidelines, and confirm that every outgoing B2B invoice carries the official signed stamp of the national registry.

Leave a Reply